Priority Alert: 2023 RS Plan Single Cash Payment Interest Rates Issued

The Internal Revenue Service has issued the interest rates used to calculate Retirement Security (RS) Plan single cash payments in 2023.

Different rates are used depending on when an employee earned benefits within the RS Plan. The GATT rate (30-year Treasury rate) generally applies to benefits earned before 2008. The Pension Protection Act (PPA) rates generally apply to benefits earned after 2007. PPA employs three rate segments in order to apply an interest rate to each annuity period that would be considered consistent with the period from retirement to the time a particular annuity payment would have been made.

As a reminder, PBGC interest rates no longer apply in the determination of RS Plan single cash payments.

Each interest rate is used in combination with a different mortality table, which can have a significant effect on the amount of the benefit as a single cash payment.

What does this mean for RS Plan participants considering retirement?

Generally, the value of a single cash payment decreases when interest rates increase. Due to the notable increase in the interest rates, the single cash payment factor for a particular age generally will be lower using the 2023 rates than using the 2022 rates.

A number of other factors affect a single cash payment, including pay, benefit service and age. This means that, while the interest rate changes listed above will most likely cause a single cash payment amount to be much lower in 2023 compared with 2022, other factors could offset some of that decrease in the amount of the single cash payment.

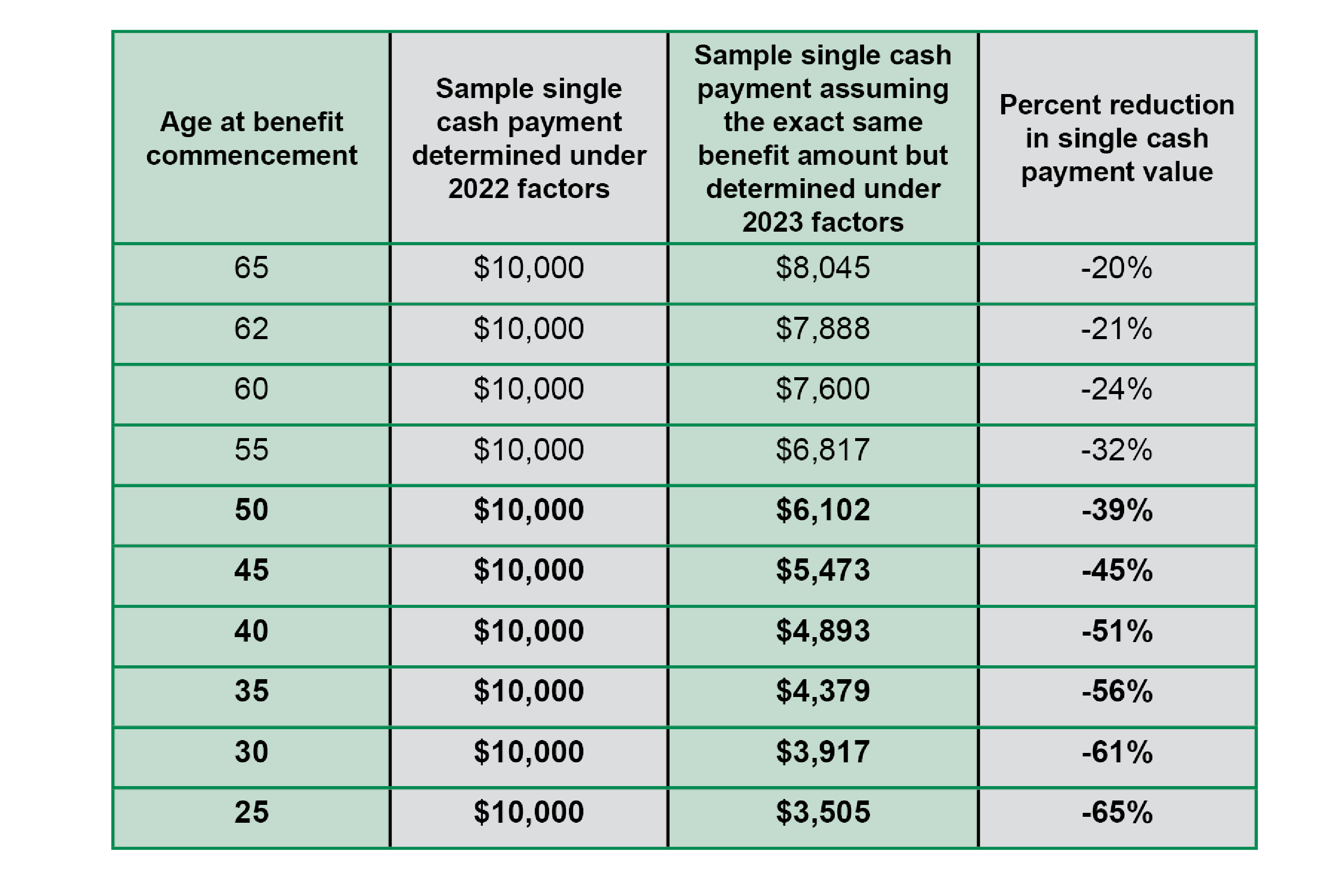

The table below shows a comparison of the value of a single cash payment as determined under the 2022 and 2023 factors, with the same accrued benefit amount used for both values shown on each row. In the second column, the benefit is set at a level that ensures the value of the single cash payment equals $10,000. Note:

- The single cash payments are determined for an age 62 normal retirement age without a cost-of-living adjustment. Reductions at each age would be slightly different under other plan designs.

- The actual difference between the values of a single cash payment for a particular person will differ depending on the proportions of their benefits payable under the GATT and PPA interest rates.

- The reductions below should be slightly less severe in practice because a benefit determined in 2023 is expected to be based on a slightly higher final average pay, and slightly higher service. The single cash payment might also be higher because the person attained their next integer age moving from 2022 to 2023.

As a reminder, benefits administrators have the ability to model and view most RS Plan benefit estimates on the Employee Benefits website. Simply go to Co-op Retirement > RS Plan Estimates. Please note: RS Plan estimates ordered through the Employee Benefits website as of December 17, will reflect the new rates.

Considering single cash payments

Participants considering taking their benefit as a single cash payment should thoughtfully review all distribution options and their personal plans for retirement income. Taking a single cash payment provides the benefit all at once, but participants must consider how they plan to save, spend or invest their benefit. Participants who choose annuity forms of payment (other than the cash refund annuity feature) are not significantly affected by these interest rate changes.

An educational flier, “The Answers You Need: Weighing Your RS Plan Payment Options,” is available for you to share with employees. This flier discusses various benefit options in the RS Plan, including a broad selection of annuity choices, and describes how a single cash payment is calculated and how fluctuations in interest rates can affect the value of a single cash payment. The flier also reminds employees to review their overall financial readiness before making final decisions about retiring. Members of NRECA’s Personal Investment & Retirement Consulting team are also available for one-on-one conversations by calling 866.673.2299, option 6, or by email at pirc@nreca.coop.

If you have questions, contact the Member Contact Center at 866.673.2299 or contactcenter@nreca.coop.