SECURE Act Provisions Change Required Minimum Distribution Rules

Signed into law on December 20, 2019, the Setting Every Community Up for Retirement (SECURE) Act contains many provisions driving changes in benefits plan administration. These provisions take effect at various dates as contained in the legislation.

NRECA will share more details as information becomes available; however, participants in both the NRECA-sponsored 401(k) Pension Plan and the Retirement Security (RS) Plan need to be aware of a change in the rules governing required minimum distributions.

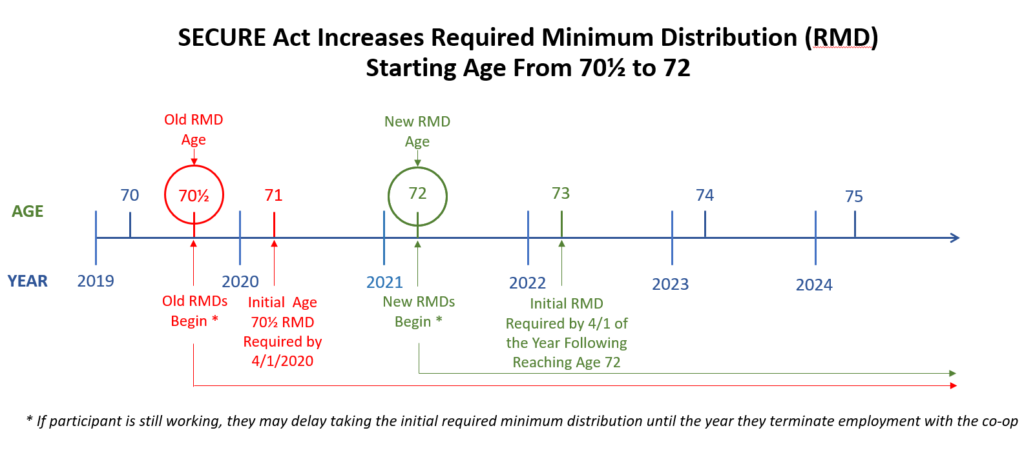

Before the SECURE Act, distributions from retirement plans had to commence by April 1 following the later of: (i) the calendar year in which the participant attained age 70½, or (ii) the calendar year in which the participant retired.

After enactment, this continues to be the rule for all participants who turned 70½ on or before December 31, 2019. For those who turn 70½ after December 31, 2019, the triggering age increases to the later of 72 or termination of employment.

Below is a snapshot of how the required minimum distribution rule applies based on a participant’s age and employment status.

In the event the participant does not request a distribution equal to the amount of the current year’s mandatory distribution amount, NRECA notifies 401(k) Plan and RS Plan participants of the required minimum distributions amount(s) for the current year. If NRECA does not receive a withdrawal request by December 1, an automatic distribution is issued by check prior to December 31. A standard 10% federal withholding tax will be applied to all required minimum distributions payments unless the participant provides a written request to waive tax withholding.

If you, or your participants, have any questions about these changes, please reach out to the NRECA Member Contact Center at 866.673.2299 and ask to be transferred to a Retirement Plan Distribution Unit representative.