IRC Section 415 Benefit Limitation Relief Measures

We are excited to announce the passage of this latest Consolidated Appropriations Act (CAA 2023), which President Biden signed into law on December 29, 2022, which brings limited relief for the impact of benefit limitations from a tax-qualified pension plan like Retirement Security (RS) Plan offered by NRECA.

The Internal Revenue Code (IRC) Section 415 benefit limitations were intended to affect only highly paid individuals by limiting their annual benefit payable to a government-mandated dollar limitation (currently $265,000 for 2023), or 100% of their average annual compensation, if lower.

Unfortunately, this current structure has resulted in the benefit reduction of certain non-highly compensated employees whose long service could produce a benefit above 100% of their average compensation, but who make far less than the dollar limitation.

CAA 2023 amends IRC Section 415 with a special provision for employees of rural electric cooperatives clarifying that the “100% of average compensation” limitation no longer applies to certain “non-highly compensated” cooperative employees (ref Division T, Title I, Sec. 119 Pages 2123 (line 3) to 2124 (Line 25)). This specific clarification is what your NRECA team has been fighting to get enacted into law.

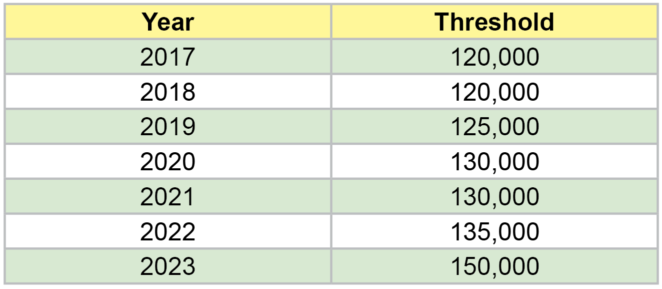

To be exempt, an RS Plan participant’s annual compensation must not exceed the annual salary thresholds under IRC Section 414(q) during the earlier of the year of termination of employment and the year they commence receiving their retirement distribution, and the five years preceding such earlier year. These are the IRC Section 414(q) thresholds for determining who is a highly compensated employee over the past several years:

NRECA is currently evaluating this brand new piece of legislation, in the absence of specific regulatory guidance, to determine how and when we can begin to apply this relief to eligible RS Plan participants. As a first step, NRECA will begin applying this relief as soon as administratively feasible to RS Plan participants who meet the eligibility criteria and are scheduled to receive their benefit distributions in 2023. As a result, some individuals with in-process or upcoming 2023 distributions may receive additional benefit payment(s) after their initial payment.

Over the coming months, we will also be reviewing potentially eligible non-highly compensated RS Plan participants with distributions initiated in 2022, that were subject to the IRC Section 415 limitation, to determine if we can retroactively apply this relief. We do not anticipate any additional cost for these retroactive adjustments. No action is required of any cooperative benefits administrator for this process; if we determine any additional information is needed to make a final determination we will contact you directly.

We hope that you are as excited about this legislative victory as we are. Look for additional registration information for a webinar on this topic in the coming weeks. In the meantime, please contact your NRECA field representative for additional information or assistance.